Risk Aversion & Value

Why Buffett might be selling Apple so he can get back to buying cigar butts

Investing involves laying out capital today, expecting a higher return in the future. Most of us would accept that the future is unknowable; therefore, investing involves risk. The history of risk is fascinating and results from two critical prerequisites that we now take for granted: first, the idea that our future is not ordained, and second, a number system capable of computation that includes a zero. Modern civilisation took centuries to arrive at the fortunate coincidence of these ideas.

As Peter Bernstein said in Against the Gods: The Remarkable Story of Risk

The word "risk" derives from the early Italian risicare, which means "to dare." In this sense, risk is a choice rather than a fate. The actions we dare to take, which depend on how free we are to make choices, are what the story of risk is all about. And that story helps define what it means to be a human being.

Today, investment professionals consider equities risky due to their price volatility compared to government bonds, which they commonly describe as risk-free. Typically, the standard measure of a portfolio's risk is its historic price volatility, frequently compared to a yardstick such as an index. Indeed, regulators usually insist that investment managers provide their investors with such relative measures of riskiness. However, relative performance to a benchmark is an industry-derived calculation that cannot be deposited into a bank account or spent.

Equity is risky. It represents the safety valve for a market or economy. A share in a company gives holders the residual rights to what remains after paying all other stakeholders. If things go badly, it takes the first loss; if nothing is left or worse, shareholders get wiped out.

A ship in the harbour is safe, but that is not what a ship was built for. John A. Shedd

However, two critical factors compensate equity holders for assuming such risk. While other stakeholders, such as employees, suppliers, landlords and lenders, are paid fixed contractual amounts, shareholders' returns are theoretically limitless. The second factor is the potential for a compounded reinvestment return on the equity residual via the company's capital allocation policy. Managers who are owners or behave like owners greatly enhance equity returns over the long term through a focused understanding of the real risks involved in their business and the best means to mitigate them.

Investors often begin as traders and learn the hard way that their circle of competence is smaller than they thought. Investors have a greater understanding of what they don't know. For Buffett,

the determinant of success is not how much you know but rather how realistically you define what you don't know.

However, successful focused investing ultimately morphs into ownership, and the pinnacle of the investment pyramid is an owner's mindset where he says,

If you aren't thinking about owning a stock for ten years, don't even think about owning it for 10 minutes.

When Buffett finds attractive businesses run by managers with an owner's mindset, he often acquires 100% of the equity.

Company founders and multigenerational owners of family businesses typically run their companies for the long term. In my experience, these owner-managers are generally uninterested in the short-term fluctuation of their equity value, as indicated by their company's share price volatility. Their focus is much more on longer-term factors determining their company's sustainability. As such, investing in companies with these characteristics offers asymmetric risk opportunities. As one specialist investor owner-managed businesses said

I would rather be a passenger on a plane where the pilot didn't come aboard wearing a parachute.

Business owners see risk as an absolute. Success requires staying in the race rather than just reaching next year's executive incentive award threshold.

Buffett famously and succinctly defined his view of risk by stating his two investment rules: Rule 1. Don't lose money, and Rule 2. Never forget rule number 1.

Buffett originally applied this principle by investing in a diversified portfolio of deep-value equities, offering investors a high safety margin between their acquired price and perceived value. He later described such opportunities in the 1940s and 50s as collecting cigar butts left on the pavement, forgotten by others, but still offering a few more puffs to whoever bothered to pick them up. He said this period of his career was the most opportunity-laden as markets recovered from the impact of two world wars interspersed with the Great Depression.

Adam Rackley of Dowgate Wealth and the manager of the Cape Wrath Fund successfully adopts this approach, which he refers to as behavioural value. He seeks to exploit investors' emotional tendency to overreact to disappointing news. Since its launch in 2016, Rackley's approach has produced sector-leading returns by taking advantage of other investors' loss aversion. Adam calls these capitulation events where human emotion overrides rationality. He is arbitraging reliably repeatable human behaviour traits to gain excess returns.

But why does this approach work? Why don't other investors and traders compete away such anomalies that the theoretical world of financial economics says should not exist?

As the name suggests, the conventional approach to analysing capital markets, the Efficient Market Hypothesis, is a hypothetical model based on a mechanistic view of how markets operate. Most people who work in the real world of listed companies, particularly the smaller, less liquid ones, will tell you it is nonsense. Why? because markets are people, and as everyone knows, we are more emotional than rational.

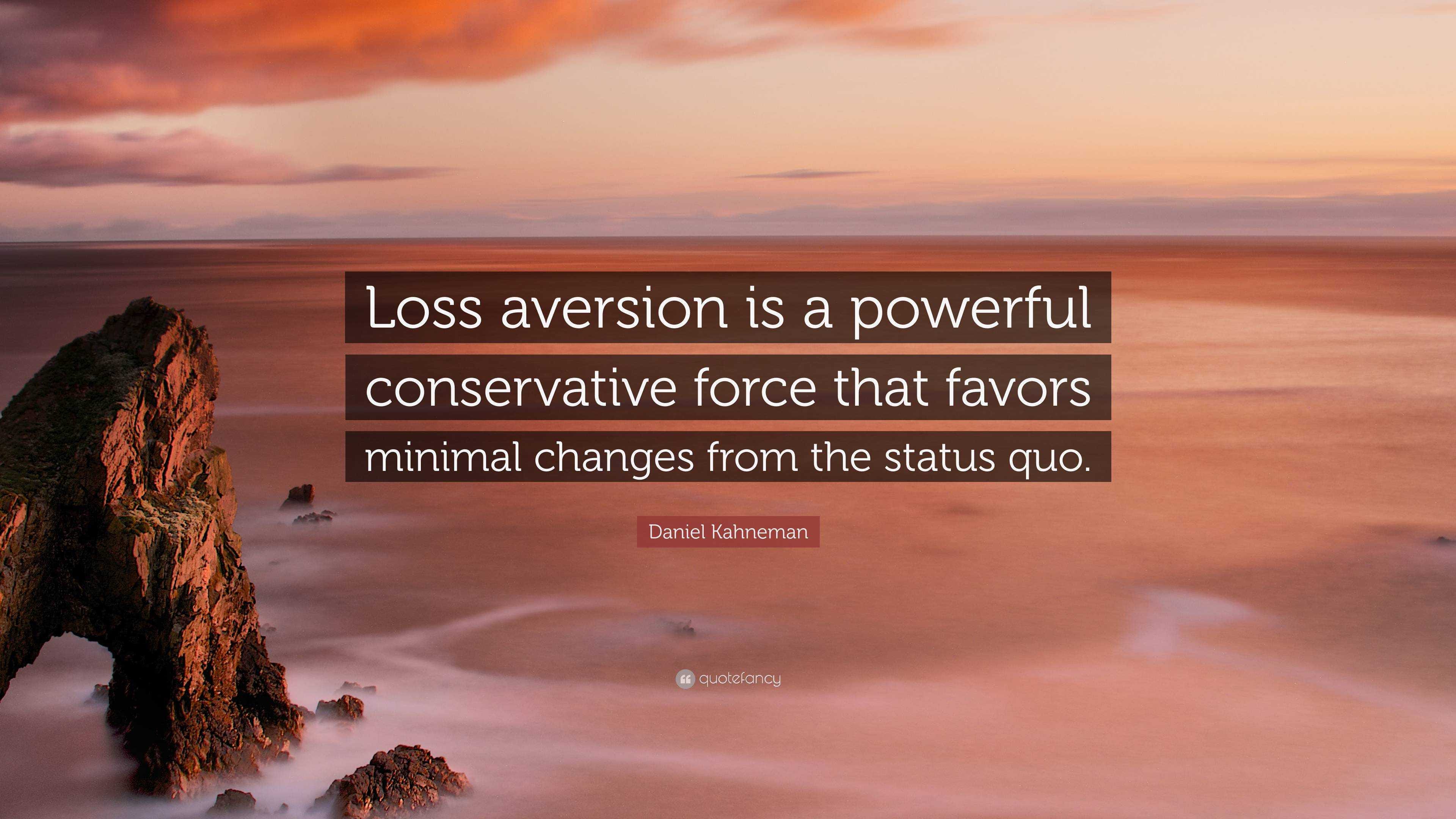

We are not just emotional. Repeated studies show that humans are twice as fearful of negative things as we feel good about positive things, what psychologists Tversky and Kahnemann called our loss or risk aversion. This discovery earned Daniel Kahnemann the Nobel Prize for Economics in 2002 (Amos Tversky had died six years earlier), a rare example of the economics profession formally celebrating a practical human behavioural rather than quantitative approach to the subject.

Of course, buying unloved deep-value equities is no get-rich-quick scheme. Canadian value investor Peter Cundhill said that

the three most important attributes for success in value investing are patience, patience, and more patience, and most investors do not possess this characteristic. Excruciating periods of underperformance are a burden that value investors must learn to endure.

However, over the long term, value investing has proven to be a highly successful strategy. Surviving the storms is critical.

Buying deep-value equities, taking advantage of consistent traits of investor irrationality, such as our innate loss aversion, has gone through periods of relative success. Buffett was picking up his cigar butt stocks in the 1940s and 50s, a period of structurally persistent inflation and high levels of government debt to GDP.

However, for most of the subsequent sixty years, characterised mainly by falling rates and benign inflation, Buffett successfully adapted the deep value strategy with the help of his long-time partner, Charlie Munger, to own quality franchise businesses at the right price. Buying prominent positions in companies like Gillette and Cocoa-Cola in the 1980s, both constituents of the growth boom Nifty-Fifty stocks typified this.

More recently, Buffett's most significant and successful investment has been Apple, a constituent of the big tech FAANGs and now Magnificent Seven AI stocks, which he has now started to sell.

Today, Berkshire Hathaway has amassed a $277bn (24%) cash position, realising $90bn from selling half of its Apple position. Many commentators are looking for the meaning of this decision. While there is usually only one reason why someone buys a share, there can be many explanations for why they might sell them. In this instance, Warren Buffett is now 93 and has recently said goodbye to his long-time partner. He may want to leave a blank sheet for the next generation of Berkshire Hathaway managers.

However, my preferred interpretation is that Buffett sees similarities between the 1940s and 50s and our current investment landscape. For example, he is acutely aware of the risks of the Yen carry trade, being one of its many participants. Government debts are back at levels last seen in his cigar butt heyday post-World War Two. US federal debt is currently $35 trillion (more than 120% of US GDP), increasing by $1 trillion every hundred days. There is little or no chance of this debt being repaid in dollars at anything close to today's real value, which helps explain the recent strength of the gold price.

Meanwhile, as peaks in global equity markets coincided with previous periods of market concentration, such as before 1929, 1974, and 2000, the mid-2020s have broad similarities. Perhaps Warren wants to see out his days looking for some more of those cigar butts.