Losing the Moron Premium

Unwinding Dr Doom's stealth QE might help

Last month, we compared the UK economy to the England football team's journey to the knockout stages of the Euros. Like the British economy, England outperformed the low expectations set by expert opinion. As suspected, the year of global elections has made the UK appear like a haven of calm and respectability in a chaotic world. Last week, the FT ran the headline Investors warm to UK equities in 'turning of tide' for unloved market. The UK is leading its European Group at a time when the top-performing US economy might be losing its stride, and China continues to send out confusing deflationary distress flares. As Ambrose Evans-Pritchard said,

It is almost a Goldilocks picture. The "forward-looking" data are on fire, foretelling a surge in pent-up business investment. Yet input cost inflation for firms has dropped to a 41-month low. You could hardly hope for a more perfect blend.

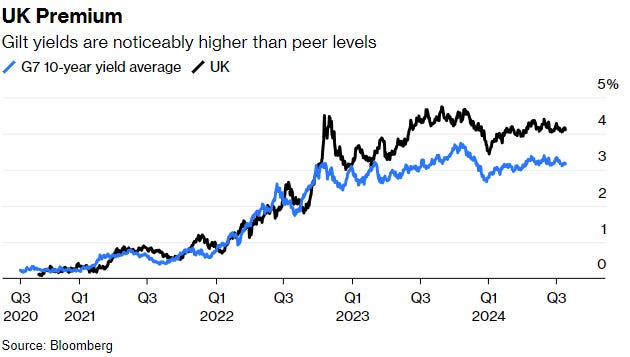

However, as the new Labour government knows, unchecked sovereign debt and unbalanced budgets challenge manifesto spending commitments. Much to the annoyance of Rachel Reeves, the Truss hangover means the UK retains its fiscal straight jacket, and its "moron premium" gilt yields persist. As Marcus Ashworth put it,

These elevated borrowing costs, dubbed the "moron risk premium," are too costly to be allowed to perpetuate but it's paramount to understand why investors charge more for lending to the UK.

Yet the recent twists and turns of the US presidential election, much of which wouldn't have been accepted for publication if submitted for a novel, have focused greater attention on the US, its economy and its stock market.

The US economy has seemed invincible over the last 18 months, able to withstand previously considered recession-inducing interest rates. However, while conflicting data abounds, whoever wins November's election will likely face a weaker economy and funding options that could make Rachel Reeves' problems look tame by comparison.

Politicians decide through their budgetary process how much taxpayers' money they intend to take compared with the proportion they will leave to be paid by future taxpayers via debt issuance. However, independent central banks are left to issue bank notes, manage credit, control the money supply, and set policy rates. Most commentators view economic policy as siloed in fiscal or monetary buckets. It is how economics is taught: fiscal policy impacts the real economy, and monetary policy affects the financial economy. But some commentators beg to differ.

Chen Zhao of Alpine Research pointed out in his paper, What Debt Crisis?

To ask where the limit is for government debt accumulation is identical to asking where the limit is for money supply for the same economy ... In the end, money and government debt are the same thing. The only differences are that they have different maturities, and holders of government paper are paid interest.

While Zhao dismisses the alarming growth in developed world sovereign debt as a systematic financial risk, his analysis reveals the inflationary risks when monetary policy comes under overt political control. More recently, an economist who 18 years ago was nicknamed Dr Doom, best known for his accurate predictions about the impending GFC in 2006, joined this debate.

Stephen Miran and Nouriel Roubini (the famed perma-bear and profit of doom), in a paper, subtitled The Tug of War Over Monetary Policy, highlight the emerging policy clash between the Fed and the US Treasury, which they call Active Treasury Issuance (ATI), otherwise known as stealth QE.

ATI is the underreported recent trend for the US Treasury to issue a larger proportion of T-Bills (notes of a year or less in duration) instead of the more usual quota of longer-maturity (2-30 yr) Treasury bonds. Miran and Roubini regard ATI as quantitative easing delivered by a politically motivated Treasury. Further, the authors calculate that,

The size of stealth QE provided to date is roughly $800 billion, equivalent in economic terms to about one percentage point of cuts to the Federal Funds rate. Contrary to the Fed's insistence that monetary conditions are restrictive, they are not, and the Treasury's issuance policies help explain the persistence of inflation and strong economic growth. Heavily relying on bill funding sets up an unattractive problem for whoever is in charge at 1500 Pennsylvania after the election: the need to term out all those bills into duration-bearing coupon securities. We expect the Treasury to have $1 trillion of excess bills by early next year.

As they say, the market only has a finite capacity to assume interest rate risk, and pushing out duration will negatively impact risk asset pricing. But it gets worse.

This ATI stimulus, intended to coincide with November's election, coincides with other chickens due home to roost. The reinstatement of the Federal debt ceiling will be in full view by January, and it is within the same budgetary period that the 2017 'temporary' Trump tax cuts expire.

Furthermore, Treasury Secretary Yellen has already exhausted the post-COVID one-time-only liquidity pool. She tapped out the Treasury General Account to extend the Federal Debt Ceiling for another 12 months. She hoovered up the Reverse Repo Reserves with her extraordinary rate of T-Bill issuance. The Treasury's emergency funds are as depleted of liquidity as the Strategic Petroleum Reserve is of hydrocarbon molecules.

Of course, this does not mean the US government will have a Truss moment. Unlike Kwarteng then and Reeves now, Secretary Yellen or her successor retain the exorbitant privilege of issuing debt denominated in the World's pristine collateral. However, the chickens returning to roost imply higher levels of Treasury debt issuance with stickier dollar interest rates and higher inflation, all other things being equal (which, of course, they never are).

What this means is that if the new Labour government plays its hand well and doesn't succumb to fully opening the public spending taps, it is in citing shot of losing the UK's "moron premium." Let's see.

The UK might not have much fiscal flex in its armoury, but it certainly has interest rate flex. As Marcus Ashworth points out in his Bloomberg column, UK real rates are at their highest level for a decade, implying scope for cuts. If the global stock market continues to rotate from big tech into less liquid small and mid-cap value stocks, the UK will continue to benefit. Doing well in its European Group could result in the UK rising up the global rankings too, but let's not get ahead of ourselves.